https://www.tuck.com/sleep-and-financial-health/

Quick Overview

Are you struggling to save up for retirement, pay off student loan debt, or simply stay on top of your monthly rent? You’re not alone. When it comes to worries that keep us up at night, financial woes consistently rank at the top.

Stress of any kind is one of the leading contributors to insomnia. Financial stress is no different. People in poor financial health are more likely to suffer from disrupted sleep, short sleep, and sleep disorders like sleep apnea.

Your financial health impacts your sleep. The reverse is also true. With poorer sleep, it’s harder to make sound economic decisions, stay productive, and cope with financial hardship. As a result, your financial health may worsen.

What’s behind the link between financial health and sleep? Below, we review the sleep issues related to financial health, and offer tips for better sleep and money management.

How Sleep Impacts Your Financial Health

Sleep and Financial Health Are Connected

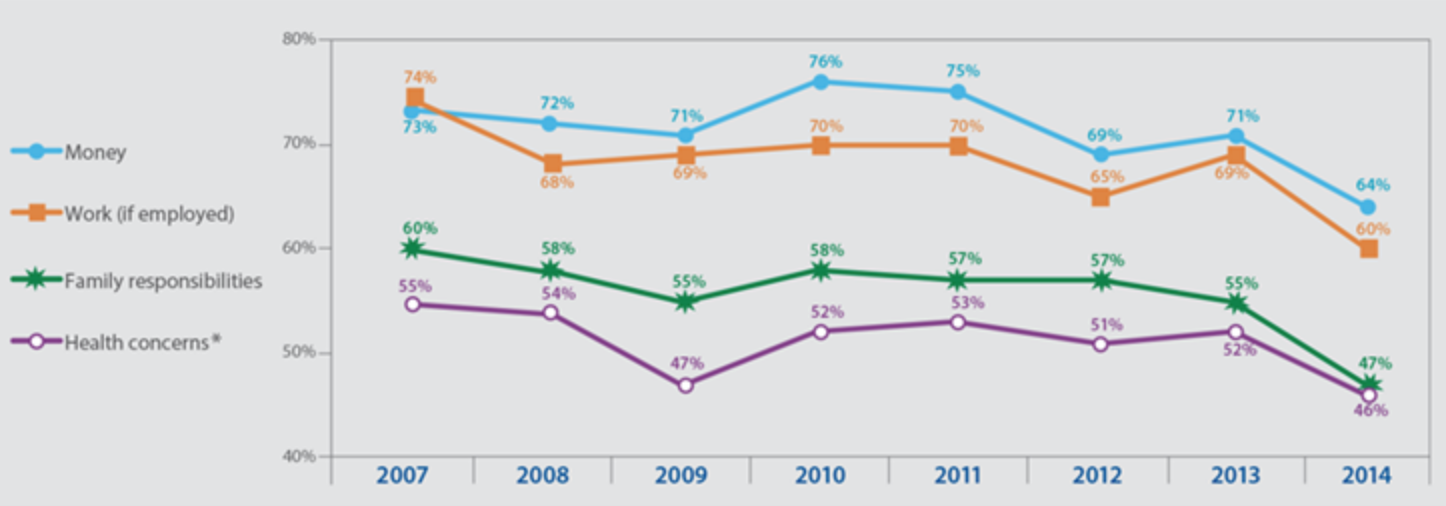

Money is the top source of stress for most Americans, according to the latest research from the American Psychological Association. One in four adults feel stressed about money all of the time, with over half having “just enough” money to make ends meet each month.

Source: APA

The prevalence of financial stress has been confirmed by several other sources. According to PwC, financial matters far surpass stress over our jobs, relationships, and health.

Sleep Disorders Associated with Poor Financial Health

On a daily basis, people who are financially stressed get less sleep than their less-stressed peers. They also have a higher risk of sleep disorders like insomnia and sleep apnea.

Insomnia describes an inability to fall or stay asleep. Symptoms include daytime sleepiness, nighttime awakenings, and low energy. Chronic insomnia, which lasts months or more, increases your risk of developing long-term health conditions like obesity, diabetes, and cardiovascular disease.

Likewise, financial stress has been linked to an increased risk of dying from a cardiovascular event, as well as contracting metabolic syndrome, a common precursor to heart disease, diabetes, and stroke.

Obstructive sleep apnea (OSA) describes a condition where the individual experiences temporary lapses in breathing while they sleep, resulting in a gasping or choking sound. Symptoms include waking up with a headache, weight gain, mood changes, and tiredness.

Individuals with OSA spend more than twice the number of days in the hospital than healthy peers. They also have nearly double the healthcare bills, amounting to an average difference of $50,000.

Either of these sleep conditions result in sleep deprivation. Sleep deprivation is what it sounds like: it describes a state of being sleep-deprived, whether that’s after an all-nighter, or missing out on just a few hours of sleep for days, months, or years.

Symptoms include trouble with memory, concentration, or focus; increased irritability, impulsivity, and mood swings; and a decrease in coordination and balance.

Finances and Mental Health

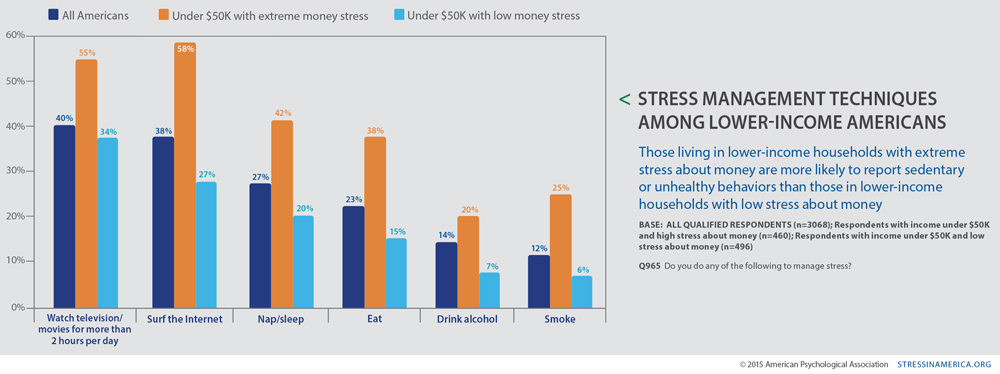

Just under 60 percent of Americans acknowledge that the state of their financial health worsens their mental health. Mental health issues are consistently linked to sleep problems, like taking longer to fall asleep and waking frequently during the night (both classic symptoms of insomnia). Reduced motivation, changes in sleeping or eating habits, and substance abuse are also warning signs.

Unfortunately, these are some of the same coping behaviors used by individuals with high financial stress, according to the APA survey cited above. For individuals with financial stress, common “unhealthy behaviors” may include (in approximate order of prevalence): watching TV for over two hours a day, surfing the internet, napping, eating, drinking alcohol, or smoking.

These folks were also more than twice as likely to describe their health as fair or poor.

Source: APA

These behaviors can all seriously interfere with the quality of your sleep.

- Alcohol and smoking are both associated with higher rates of sleep-related breathing disorders, and reduced quality of sleep.

- Binge-watching television or surfing the internet requires the use of electronic devices. These flood your brain with the same blue light your brain perceives as sunlight, delaying melatonin production and your ability to fall asleep.

- Napping seems like it’d be good for sleep, but overindulging in daytime naps can reduce your ability to sleep at night, leading to insomnia.

- Like alcohol and smoking, obesity is equated with breathing disorders like sleep apnea. Independent of obesity or weight gain, binge-eating can also double the risk of sleep problems.

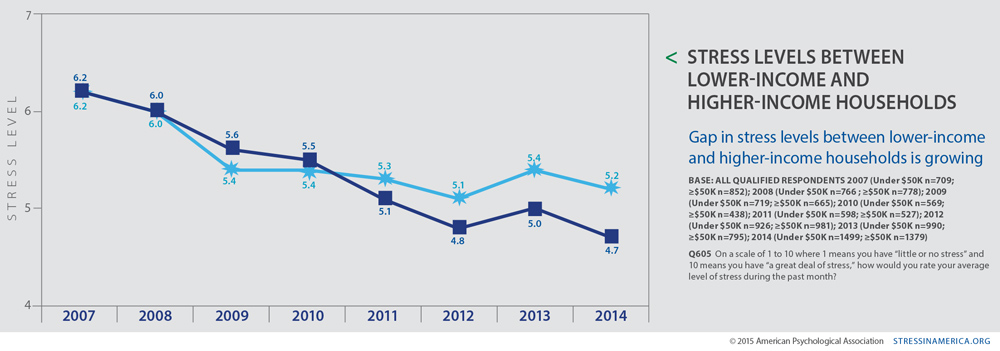

Income and Socioeconomic Stressors

Since the 2008 recession, the income gap between those who stress about money and those who don’t has widened. Only 18 percent of adults in higher-income households feel constantly stressed about money, compared with 36 percent of adults in lower-income households.Source: APA

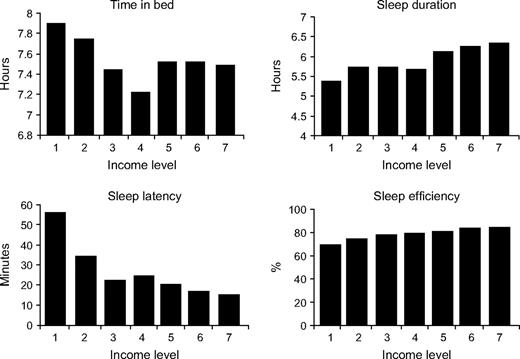

Lower-income households are also more likely to regularly miss out on sleep. The CDC has charted a linear relationship between poverty status and sleep loss, as have numerous other studies. For example, one study found that the individuals making below $16,000 (Income Level 1 in the charts, below) can spend up to three times longer trying to fall asleep than those making $100,000 or more (Income Level 7).Source: American Journal of Epidemiology

A similar trend held true for racial and ethnic minorities. In fact, some studies have found that racial discrimination alone can be a stressor that leads to disturbed sleep.

These sleep differences may also be explained by conditions common to lower-income households and socioeconomic status, such as noisier and more crowded neighborhoods. Beyond financial stress, those living below the poverty line may also have food insecurity, which has similarly been correlated with fragmented sleep.

Why Sleep Impacts Financial Health

Financial stress makes it hard to fall asleep at night. Over time, those restless nights create a state of sleep deprivation, which in turn, impacts your ability to manage your finances wisely. Below, we review the mechanics of this vicious cycle, primarily through the effects of sleep deprivation on your cognitive performance and decision-making skills.

Reduced Cognitive Performance

Sleep deprivation negatively affects your cognitive performance, resulting in:

- Reduced attention and focus

- Slower reaction times

- Decreased ability to learn and commit learnings to memory

- Decline in short-term recall

- Increased errors and forgetfulness

- Microsleeps

All of these are bad enough on their own. Worse, sleep-deprived individuals have to expend even more effort, simply trying to be as functional as they would be after a full night’s rest. Further, when they do perform tasks well, their ability to do so swiftly declines the longer they keep working.

Plus, studies frequently find that individuals remain unaware of their sleep deprivation, so they may not even realize they’re making mistakes.

It’s common for people to see a list like this and shrug it off, assuming that the odd sleepless night or a few weeks without great sleep shouldn’t make too much of a difference. This only becomes a problem when it’s a chronic issue, right? Wrong.

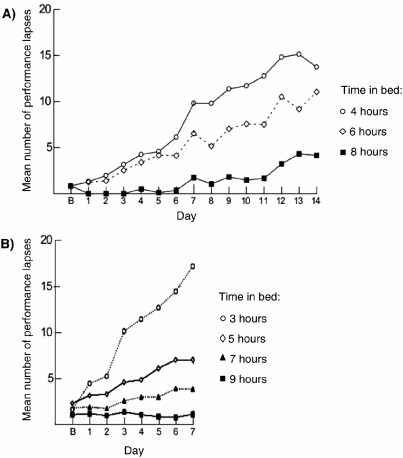

These issues present after just one night of short sleep. That means that if you get less than the recommended seven hours of sleep for adults, you can expect to be as cognitively impaired as you would be if you had pulled an all-nighter.

One study found that the performance impairment of a group who slept six hours or less per night was equivalent to those who didn’t sleep at all for two nights in a row. That’s only a difference of one hour.

Unfortunately, this kind of chronic sleep deprivation is common. According to the CDC, about one-third of Americans experience this short sleep on a regular basis. The longer you stick to a short sleep schedule, the worse you can expect to perform as time goes on:Source: Sleep

Impacts in the Workplace

For workers, the cumulative effects of sleep depression often result in absenteeism or presenteeism. Presenteeism refers to those who come to work when they’re ill or fatigued, so they’re not able to perform at normal levels. They may be at work, but they’re not truly present. Researchers estimate the lack of productivity due to sleep deprivation could be costing the U.S. economy as much as $411 billion.

At a more personal level, these cognitive impairments can take a toll on your financial health. An impaired ability to remember things and stay focused makes you less effective at work, reducing your chances of getting a raise or achieving quarterly goals and bonuses.

Eventually, your productivity may be so reduced that you have to work longer hours, creating more stress and exhaustion. You may accidentally fall asleep during meetings, which your colleagues may interpret as you not caring about your job.

Increased errors at work can lead to poor performance reviews or job loss. Those who have physical jobs, like construction workers and others who use their hands to operate equipment, can be at particular risk. Workers with severe insomnia are 70 percent more likely to incur a work-related injury than their better-sleeping colleagues, and disturbed sleep nearly doubles the risk of dying in a workplace accident.

Impaired Judgment and Decision-Making

Cognitive impairments can have an impact outside of the workplace, as well. Sleep-deprived individuals are prone to rash judgment, poor decision-making, and increased risk-taking.

When you’re sleep-deprived, you may be more likely to make impulse purchases, or have a tougher time convincing yourself to stick to your budget. You may feel so exhausted that you make big purchases quickly, without taking time to shop around for the best deal.

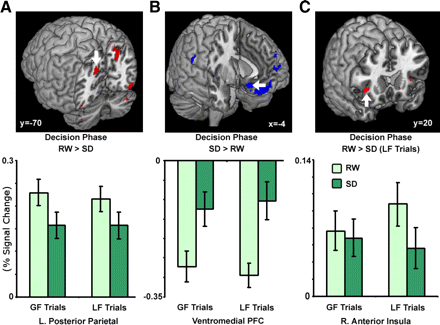

One intriguing study from 2011 found that sleep loss impacts your brain’s ability to accurately assess economic consequences. When you make decisions while sleep-deprived, brain activity increases in the areas that process positive outcomes, and decreases in the areas that process negative outcomes.

In other words, a sleep-deprived brain is so attracted to an opportunity of monetary gain, that it’s less able to consider the potential negative consequences of an economic decision.“Even if someone makes very sound, risky financial decisions after a normal night of sleep, there is no guarantee that this same person will not expose you to untoward risk if sleep deprived.”

– study co-author Michael Chee, M.D., Journal of Neuroscience

The researchers were able to observe these changes in the participants’ brain activity. In the images below, RW stands for “rested wakefulness” and SD stands for “sleep deprivation.”Source: Journal of Neuroscience

How to Improve Your Sleep and Financial Health

If you’re struggling to improve your finances, the key may not be pushing yourself to the edge. Paradoxically, it may be as simple as getting more sleep. According to one study, increasing your average weekly sleep by just one hour could lead to a 5 percent increase in income.

Below, we share tips for getting a better handle on your finances, and your sleep.

1. Map Out Your Finances.

Sometimes, anxiety over money intensifies due to a nebulous fear of “not making enough,” even for those who make the most. When the unknown becomes known, it often becomes less frightening.

Sit down and take account of your finances and your financial goals. Then, chart out the income you need to earn, and the savings you need to build, in order to reach those financial goals. This process gives you back a sense of control over your finances, helping you feel more confident and less fearful.

2. Reduce Your Expenses.

The above process will likely point out areas where you can spend less money. Common culprits include eating out, entertainment, apparel, and consumer goods. Make a commitment to spend less in these categories, and immediately raise cash by selling items you no longer use.

Late fees can be another common, and unnecessary, expense. Save yourself time, money, and stress by setting up your bills to auto-pay.

3. Eat Better and Exercise.

Instead of overspending on restaurants, opt for healthier meals at home. A healthy diet makes for healthier sleep, and a healthier body overall — reducing your chances of costly illness and insurance claims. Good foods for sleep include leafy greens, cheese, eggs, nuts, fish, and beans. For deeper sleep, avoid eating anything too spicy, sugary, or heavy before bed. Likewise, limit your caffeine and alcohol consumption.

Pair your better diet with a regular exercise routine, too. Exercising regularly, particularly in the morning, helps tire you out by nighttime. It’s also a good stress management technique. Free forms of exercise include running, walking, or practicing yoga at home.

4. Build Your Savings.

Building up your savings relieves financial insecurity and helps you achieve your financial goals faster. If you’re worried about retirement, start contributing to your employer’s 401(k) plan or set up an independent retirement savings account.

Experts recommend putting away at least 10 percent of your income into a retirement plan. If that’s not feasible today, start with 1 percent, then make a plan to increase it every six months or every year until you reach 10 percent.

Worried about losing your job or a financial loss? Build up a rainy day fund. Decide on a number, whether it’s $25 or $100, and automatically transfer it to a savings account each month.

5. Stay on Track with To-Do Lists.

Each night, before you go to bed, write down any financial worries you have. Taking them out of your head and onto a piece of paper helps you clear them from your mind, making it easier to fall asleep. Then, write out a to-do list with special attention to the tasks you can complete the following day to improve or maintain your financial health. This process has been scientifically proven to speed up the time it takes you to fall asleep.

6. Sleep Like a Pro.

Now that you’ve organized your finances, take the time to organize your sleep. Set a sleep and wake time, and follow them religiously each day. Going to sleep at differing times disrupts your circadian rhythms, making it harder to get regular sleep.

Treat bedtime seriously. Keep your bedroom dark, cool, and quiet. Take 30 minutes before bed to complete your financial to-do list, and prepare yourself for sleep. Calm yourself with soft music, reading, or meditation. Avoid using electronics.

Final Thoughts

Your personal financial health seems like a matter of money management. But, financial health doesn’t exist in a vacuum. The quality of your sleep directly impacts your ability to manage your finances wisely.

Poor sleep impairs your cognitive performance, judgment, and decision-making skills, reducing your ability to earn an income and make sound financial decisions. Sleep loss also profoundly affects various aspects of your overall physical health, many of which compound one another and contribute to more financial health problems.

On the other hand, good sleep supports improved productivity, focus, and all-around well-being. You’re better equipped to cope with financial stress, stick to your budget, and reach your financial goals.

Avoid the consequences of sleep loss by making a commitment to stronger financial health. Start with the tips above: mapping out your goals, reducing expenses, and building your savings. Then, stay on track with to-do lists and better sleep habits.

Additional Tuck Resources

Learn more about finances and sleep at the links below.

Reblogged this on Ace Group .

LikeLike